《會(huì)計(jì)學(xué)——企業(yè)決策的基礎(chǔ) 第15版(英文版)第六單元課后習(xí)題答案》由會(huì)員分享���,可在線(xiàn)閱讀,更多相關(guān)《會(huì)計(jì)學(xué)——企業(yè)決策的基礎(chǔ) 第15版(英文版)第六單元課后習(xí)題答案(6頁(yè)珍藏版)》請(qǐng)?jiān)谘b配圖網(wǎng)上搜索��。

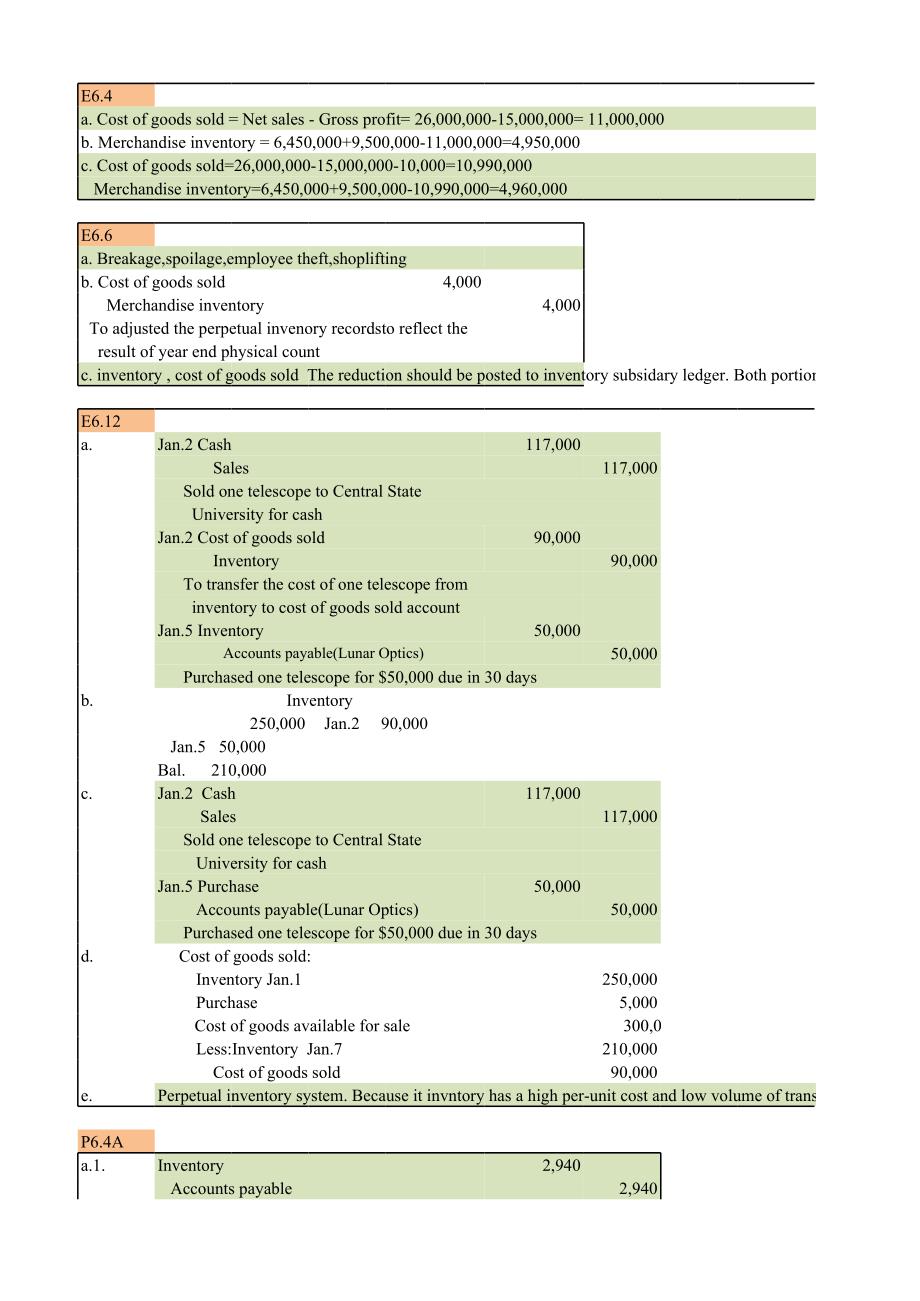

1���、E6.4a.Cost of goods sold=Net sales-Gross profit=26,000,000-15,000,000=11,000,000b.Merchandise inventory=6,450,000+9,500,000-11,000,000=4,950,000c.Cost of goods sold=26,000,000-15,000,000-10,000=10,990,000 Merchandise inventory=6,450,000+9,500,000-10,990,000=4,960,000E6.6a.Breakage,spoilage,employee

2���、theft,shopliftingb.Cost of goods sold4,000 Merchandise inventory4,000 To adjusted the perpetual invenory recordsto reflect the result of year end physical countc.inventory,cost of goods sold The reduction should be posted to inventory subsidary ledger.Both portions should be posted to genenral ledge

3、rE6.12a.Jan.2 Cash117,000 Sales117,000 Sold one telescope to Central State University for cashJan.2 Cost of goods sold90,000 Inventory90,000 To transfer the cost of one telescope from inventory to cost of goods sold accountJan.5 Inventory50,000 Accounts payable(Lunar Optics)50,000 Purchased one tele

4����、scope for$50,000 due in 30 daysb.Inventory250,000 Jan.2 90,000 Jan.5 50,000Bal.210,000c.Jan.2 Cash117,000 Sales117,000 Sold one telescope to Central State University for cashJan.5 Purchase50,000 Accounts payable(Lunar Optics)50,000 Purchased one telescope for$50,000 due in 30 daysd.Cost of goods sol

5、d:Inventory Jan.1250,000 Purchase5,000 Cost of goods available for sale 300,000 Less:Inventory Jan.7210,000 Cost of goods sold90,000e.Perpetual inventory system.Because it invntory has a high per-unit cost and low volume of transactions.P6.4Aa.1.Inventory2,940 Accounts payable2,940To record purchase

6�����、 of 10 televisions at net costJan.15 cash450 Sales450 Sold cost of goods sold294 Invenory294Jun.20 Accounts payable 2,940 Cash2,940a.2.Jun.10 Inventory3,000 Accounts payable3,000To record purchase of 10 televisions at gross invoice priceJan.15 cash300 Sales300 Sold cost of goods sold450 Invenory450J

7、un.20 Accounts payable3,000 Cash2,940 Purchase discount taken60b.1.Accounts payable2,940Purchase discounts lost60 Cash3,000To record payment of invoice after expiration of the discount periodb.2.Accounts payable3,000 Cash3,000To record payment of invoice after expiration of the discount periodc.Net

8����、cost.Because the purchase discount lost account could brings to managements attention any failure to take advantage of the cash discount offered by suppliers.P6.8Aa.The series of transactions through which a business generaes its revenue and its cash recipts from customers.Assets:Invetory,Accounts r

9、eceivable,Invenory Liabilities:Accounts payableb.Jan.2 Inventory24,250 Accounts payable(Sharp)24,250 Purchase 20 modems and 80printers at net cost.Payment due in 60 days.Jan.6 Accounts receivable(Pace Cor.)10,000 Sales10,000 Sold 30 products to Pace Corporation on account.payment due in 90 days Cost

10�、 of goods sold6,100 Inventory6,100 To transfer the cost of 30 products from Inventory to cost of goods sold accountc.Beginning inventory500,000Add:Purchases24,250Inventory avaliable for sale524,250Less:Cost of goods sold6,100Ending inventory518,150d.Jan.2 Inventory24,250 Accounts payable(Sharp)24,25

11、0 Purchase 20 modems and 80printers at net cost.Payment due in 60 days.Jan.6 Accounts receivable(Pace Cor.)10,000 Sales10,000 Sold 30 products to Pace Corporation on account.payment due in 90 dayse.Beginning inventory500,000Add:Purchases24,250Cost of goods available for sale524,250Less:Ending invent

12����、ory518,150Cost of goods sold6,100f.Periodic.It inventory with many different kinds of low cost items.Has high volume of sales transactions.g.Gross profit=Net sales-Cost of sales=10,000-6,100=3,900Gross profit margin=Gross profit/Net sales=3,900/10,000=39%c.inventory,cost of goods sold The reduction

13、should be posted to inventory subsidary ledger.Both portions should be posted to genenral ledgerPerpetual inventory system.Because it invntory has a high per-unit cost and low volume of transactions.The series of transactions through which a business generaes its revenue and its cash recipts from customers.

會(huì)計(jì)學(xué)——企業(yè)決策的基礎(chǔ) 第15版(英文版)第六單元課后習(xí)題答案

會(huì)計(jì)學(xué)——企業(yè)決策的基礎(chǔ) 第15版(英文版)第六單元課后習(xí)題答案